Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

In Australia, retirement is not strictly defined by the government in a one-size-fits-all manner. Instead, retirement is generally considered to be the point at which a person decides to cease full-time work and withdraw from the workforce. The age at which individuals can access their retirement benefits, such as the age pension and superannuation (retirement savings), varies.

The average retirement age in Australia can vary depending on various factors such as health, financial situation, and personal choice. However, according to the Australian Bureau of Statistics, as of 2023, the average retirement age for Australians was around 64. Notably, these are averages and individual circumstances can greatly influence the actual age of retirement.

Recent trends indicate the average retirement age in Australia is increasing due to a variety of factors including increased life expectancy, changes in government policy, and economic conditions.

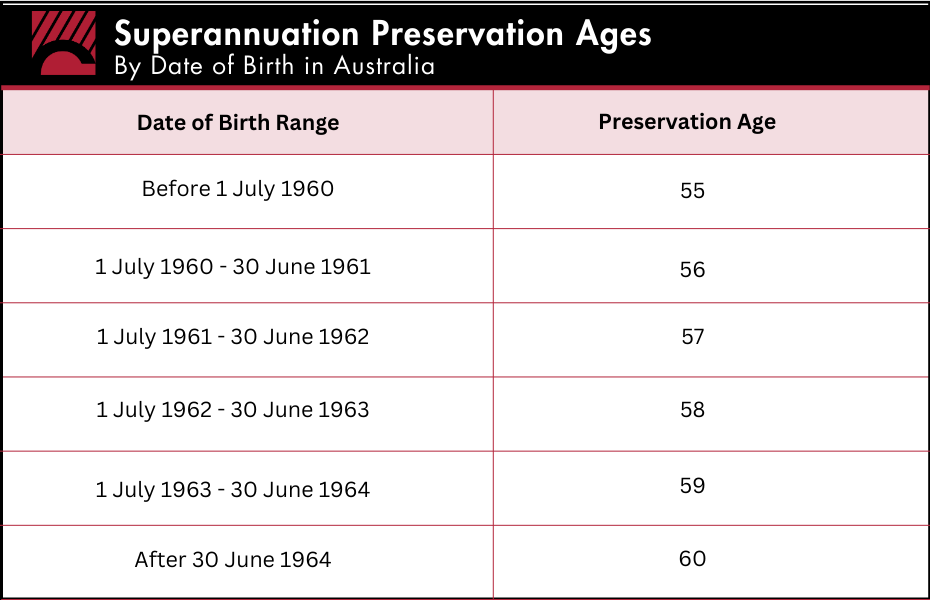

Preservation age is the minimum age at which you can access your superannuation benefits, contingent upon meeting a condition of release, such as retirement. The birth preservation age in Australia varies based on your date of birth, as outlined below:

It's crucial to highlight that merely reaching your preservation age does not automatically grant access to your super. Typically, you must have also retired or satisfied another condition of release.

Understanding your birth preservation age is integral, especially considering the average age at which Australians retire. By aligning your plans with the broader landscape of the Australian retirement age, you can navigate superannuation access with informed decision-making.

When contemplating retirement, several key factors might be considered:

Determining the right retirement age involves understanding your preservation age (55 to 60) and considering how superannuation taxes impact your plans. Early withdrawal before 60 may incur taxes.

'Good leaver' conditions in an employee share scheme can shape your retirement trajectory, allowing continued benefits post-departure for retirement. This consideration is vital for those aspiring to a comfortable retirement.

Small business owners may benefit from a retirement capital gains tax concession, influencing the timing of their retirement decision. These are general factors, and seeking personalised advice is essential for tailored retirement planning that considers individual circumstances.

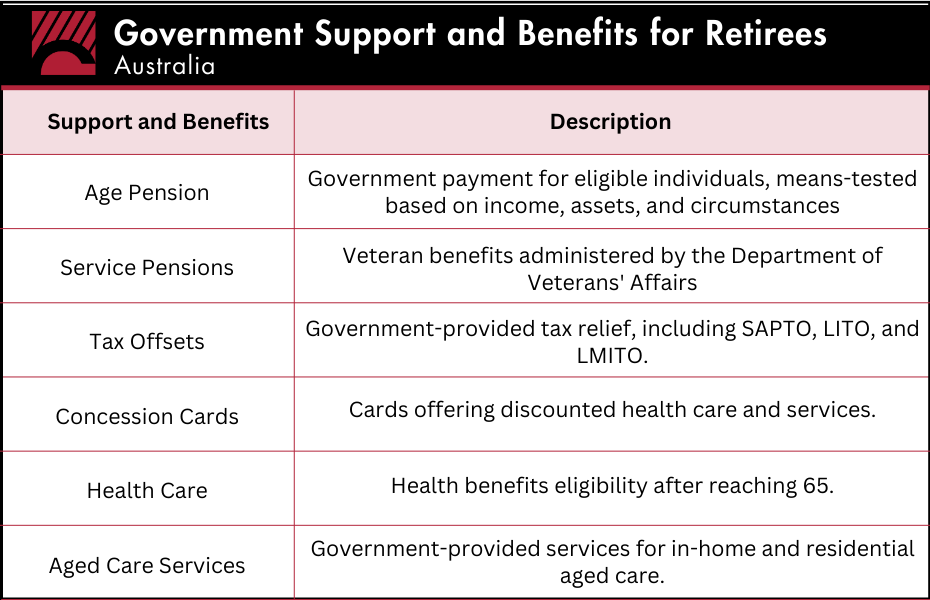

The age pension, a regular government payment, is distributed to individuals who have reached the eligible age. This financial assistance undergoes means-testing, considering income, assets, and relevant circumstances for both you and your partner in determining pension payments.

Veterans, including eligible partners, widows, and widowers, receive benefits based on age or disability, administered by the Department of Veterans' Affairs. Understanding these benefits is crucial for financial planning, encompassing considerations like age pension, pension payments, and their potential as an income stream within the broader context of personal objectives.

The Australian government provides several tax offsets that you may be eligible for in retirement, such as the Seniors and Pensioners Tax Offset (SAPTO) and the Low Income Tax Offset (LITO).

The government provides different types of concession cards that can give you cheaper health care and some discounts.

Once you reach the age of 65, you may be eligible for various health benefits through the Commonwealth Seniors Health Card or the Health Care Card.

The government provides a range of aged care services, including in-home care and residential aged care.

Services Australia is an Australian Government agency that delivers a range of health, social, and welfare payments and services. For retirees, Services Australia plays a crucial role in providing access to and information about various government benefits and support.

Some of the key responsibilities of Services Australia include:

Please note while Services Australia provides these services, the Australian Taxation Office (ATO) is responsible for administering Australia's tax laws and managing the Australian Business Register.

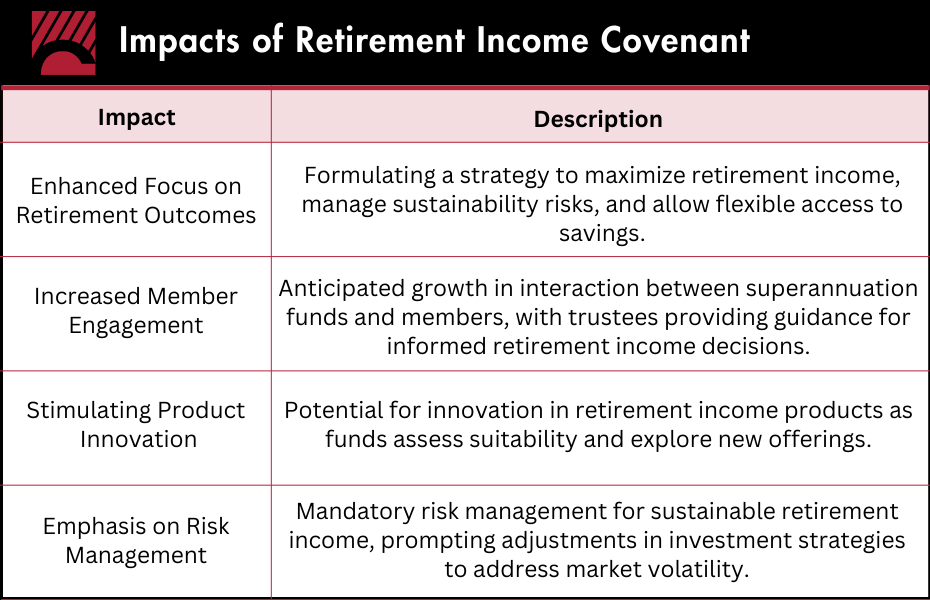

The retirement income covenant is a legislative requirement for Australian superannuation trustees, which mandates the formulation and regular review of a strategy to assist members in achieving retirement income goals. Trustees are obligated to outline how they plan to maximise retirement income, manage risks, and provide flexible access to savings during retirement. The purpose of the covenant is to improve individual retirement outcomes by ensuring thorough consideration and planning for members' needs.

The retirement income covenant is expected to have a significant impact on retirement strategies in several ways:

Trustees must formulate a strategy focusing on maximising retirement income, managing sustainability risks, and allowing flexible access to savings.

Anticipated growth in interaction between superannuation funds and members, with trustees providing guidance for informed retirement income decisions.

Potential for innovation in retirement income products as funds assess suitability and explore the development of new offerings.

Trustees mandated to assess and manage risks to members' retirement income sustainability, potentially prompting adjustments in investment strategies to mitigate market volatility.

The Trans-Tasman Retirement Savings Portability Scheme, active since 1 July 2013, facilitates the transfer of retirement savings between Australia and New Zealand for individuals relocating.

Key features include the consolidation of savings in the country of residence, ensuring no loss of associated benefits or protections, offering flexibility for those working in both countries, potential cost reduction through consolidation, and preservation of savings until reaching retirement age in the holding country. However, it's crucial to note not all Australian super funds accept transfers from New Zealand, and there are limitations on the use of transferred amounts, such as restrictions on purchasing a first home or moving to a third country.

For individuals aged 55 or older, the Australian Taxation Office (ATO) allows a potential contribution of up to $300,000 from the proceeds of a home sale into their superannuation fund. This downsizer contribution, categorised as non-concessional, doesn't impact the contribution cap, but it does factor into the transfer balance cap when transitioning super savings into the retirement phase. While it doesn't immediately affect the total superannuation balance, it's advisable to seek independent financial advice regarding its implications on age pension asset tests.

For comprehensive and professional guidance tailored to your unique situation, we encourage you to contact us. Our team is ready to offer expert advice, ensuring clarity and compliance with Australian tax regulations.

Causbrooks gives you a client manager supported by a team of knowledgeable small business experts. We’re here to take the guesswork out of running your own business.

Get in touch with us to set up a consultation or use the contact form on this page to inquire whether our services are right for you.

Any advice contained in this document is general advice only and does not take into consideration the reader’s personal circumstances. Any reference to the reader’s actual circumstances is coincidental. To avoid making a decision not appropriate to you, the content should not be relied upon or act as a substitute for receiving financial advice suitable to your circumstances.

Contact us today to learn more about how our accounting services can benefit your business. We look forward to hearing from you and helping you achieve financial success!