Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Using the bring forward rule (also referred to as the bring forward arrangement) allows you to boost your super contributions, specifically your bring forward non-concessional contributions, in a more compressed timeframe. There are specific guidelines related to age, previous non-concessional contributions, and the amount already in your super balance, often referred to as the transfer balance cap. These criteria determine your eligibility to leverage the bring forward rule.

Grasping these rules is crucial to prevent over-contributing, known as excess contributions, which could result in additional tax.

The non-concessional contributions cap is how much money you can put into your super from your after-tax income without paying extra tax. Starting 1 July 2021, you can put up to $110,000 each year. This amount changes sometimes based on average pay (AWOTE). If you put in more than the cap, you might have to pay extra tax.

Here's a list of the non-concessional cap amounts since the 201-19 financial year:

If you make contributions above the annual non-concessional contributions cap you may be eligible to automatically access future year caps. This is known as the bring-forward arrangement. It allows you to make extra non-concessional contributions without having to pay extra tax, if you meet certain eligibility conditions. If your total super balance is equal to or more than the general transfer balance cap ($1.7 million from 2021–22, $1.9 million from 2023–24) at the end of the previous financial year, your non-concessional contributions cap is nil ($0) for the current financial year.

Both the carry forward rule and the bring forward rule pertain to superannuation contributions, but they cater to different kinds of contributions and operate distinctively.

The carry forward rule is linked to concessional (or before-tax) contributions. If your total super balance is under $500,000, this rule lets you carry over the unused concessional contributions cap on a five-year rolling basis. Essentially, if you don't max out your concessional contributions cap in a specific year, you have the option to roll over the unused portion and apply it in an upcoming year.

Conversely, the bring forward rule deals with non-concessional (or after-tax) contributions. This rule allows individuals below 75 years of age to make a large contribution in one year by advancing their cap from the succeeding two years. This translates to the ability to contribute threefold the yearly non-concessional contributions cap within a single year.

To sum it up, the carry forward rule allows you to roll over unused concessional contribution limits to future years, while the bring forward rule permits you to pre-use your upcoming non-concessional contribution caps.

In summary, the bring forward rule is beneficial for individuals like Jane who are looking to maximise their super contributions in a tax-effective manner, especially as they near retirement and have access to larger sums of money to invest.

To use the bring forward rule, a person needs to be younger than 75 years old on the previous 1st of July. Also, any Non-Concessional Contributions (NCC) should be made within 28 days after the month they turn 75.

During the second year (or third year, if applicable) of the bring-forward period, your Total Super Balance (TSB) needs to be under the general Transfer Balance Cap (TBC) as of the 30 June of the previous financial year for you to make extra Non-Concessional Contributions (NCCs). An interesting point to note is that you can still contribute the remaining amount from their NCC bring-forward, even if this makes your TSB go over the general TBC afterward. That's because the main condition is for the TSB to have been below the general TBC on the last 30 June to add more NCCs within the bring-forward limit.

If the yearly NCC cap goes up because of indexation, it doesn't mean someone can contribute more under a bring-forward period they already started. This is because the bring-forward NCC limit is set by doubling (or tripling) the yearly cap from the year it began.

There could be new chances to contribute in 2023/24 for those who began the 3-year bring-forward in 2021/22 but couldn't use the full amount in 2022/23. This situation could happen if your TSB on 30 June 2022 was at or above the general TBC (which was $1.7m in 2022/23). Since the general TBC will rise to $1.9m in 2023/24, you could contribute more if your TSB on 30 June 2023 was less than $1.9m.

The ATO is in charge of handling contribution data, which includes details about the bring-forward rule. Super fund trustees don't have to decide if a contribution is allowed. However, they do report personal contributions to the ATO. If someone makes a Non-Concessional Contribution (NCC) that goes beyond the set limit based on caps and their Total Super Balance (TSB), this becomes an excess NCC. In such a case, the ATO will notify the client with an excess notice of assessment.

Individuals can view their contribution and bring-forward details by logging into myGov. From there, they can download a report to either print or email to their financial adviser. However, it's essential to be cautious when using this information. It might not show the current TSB because of how long it takes funds to report. The smartest approach would be to keep thorough records and double-check with all of the client's funds to ensure the information is accurate.

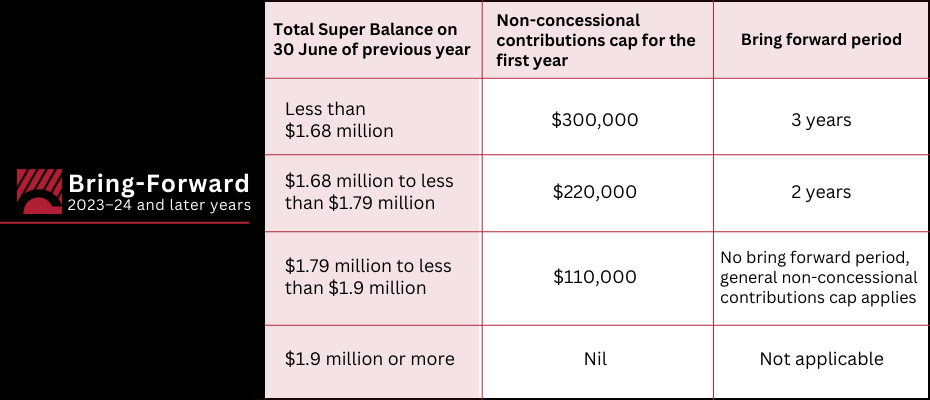

The amount you're allowed to contribute using the bring-forward rule depends on your TSB from the end of the previous financial year:

These limits reflect the non-concessional cap set at $110,000 and the general transfer balance cap of $1.9 million.

Upon activating the bring-forward rule:

Starting from the 2017–18 financial year, if your TSB equals or surpasses the general transfer balance cap by the end of 30 June of the preceding year, the remaining cap for the second or third year of the bring-forward period drops to zero.

To avoid unintentionally setting off the bring-forward rule, consider all non-concessional contributions made to all your super funds. Additionally, unreleased excess concessional contributions count towards the non-concessional cap.

The tables below summarise the bring-forward caps that apply in the first year, based on your total super balance.

If you're thinking about adding a big amount to your super, it's important to first check your ATO online services account to see if you've started a bring-forward arrangement.

To do this: log in to ATO online services, click on "Super," then go to "Information," and finally select "Bring-forward arrangement."

However, keep in mind the most recent data might not always be available on ATO online services because of how long it takes funds, especially SMSFs, to report. For the latest updates, it's a good idea to reach out to your super fund.

Causbrooks gives you a client manager supported by a team of knowledgeable small business experts. We’re here to take the guesswork out of running your own business.

Get in touch with us to set up a consultation or use the contact form on this page to inquire whether our services are right for you.

Any advice contained in this document is general advice only and does not take into consideration the reader’s personal circumstances. Any reference to the reader’s actual circumstances is coincidental. To avoid making a decision not appropriate to you, the content should not be relied upon or act as a substitute for receiving financial advice suitable to your circumstances.

Contact us today to learn more about how our accounting services can benefit your business. We look forward to hearing from you and helping you achieve financial success!